Nearly every year, the IRS quietly adjusts tax brackets and the standard deduction.

And every year, most people ignore it.

But if you’re a 1099 worker, freelancer, creator, or small business owner, these updates are not trivial. They directly affect:

- How much you should set aside

- Whether you owe quarterly payments

- Whether you qualify for certain credits

- And how aggressively you should plan deductions

Let’s break this down in plain English.

First: Why Do Tax Brackets Change Every Year?

The IRS adjusts tax brackets and the standard deduction for inflation.

This prevents “bracket creep,” where you earn slightly more due to inflation but get pushed into a higher tax bracket without actually having more buying power.

In short: The updates are designed to keep your taxes fair relative to inflation.

But “fair” doesn’t mean you won’t owe more.

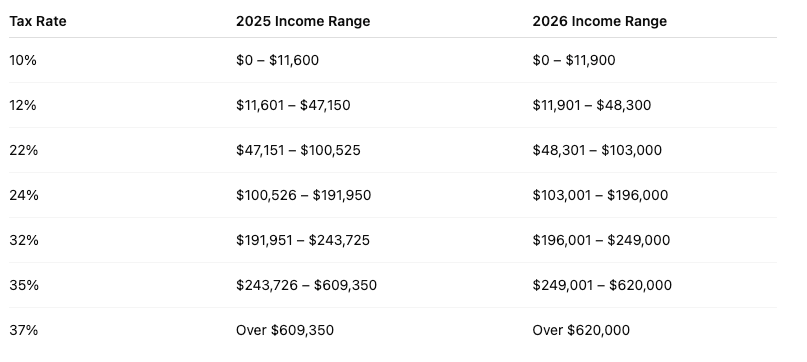

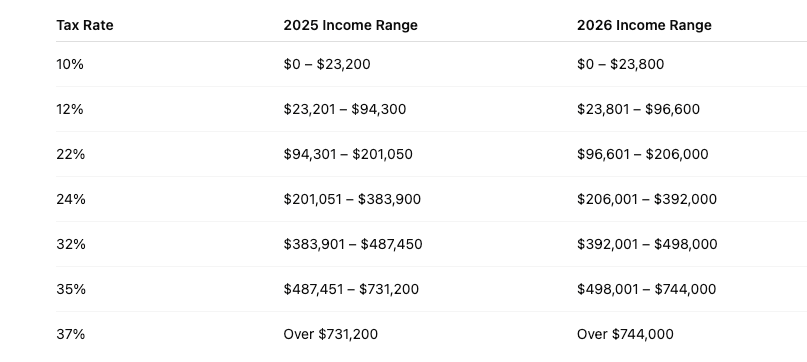

2025 vs 2026 Tax Brackets

Single Filers

Married Filing Jointly

What Actually Changed?

Notice:

- The rates didn’t change.

- The income thresholds increased slightly.

- This means you can earn a little more before moving into the next bracket.

For most people, the change is modest, often a few hundred dollars to a couple thousand dollars of additional room in each bracket.

2026 Standard Deduction: What It Means

The standard deduction is the automatic income reduction you get before taxes are calculated.

You either:

- Take the standard deduction, or

- Itemize deductions (whichever is higher)

When the standard deduction increases:

- Less of your income is taxable.

- You may not need to itemize.

- Your overall tax bill could decrease slightly.

For most 1099 workers, especially those early in business, the standard deduction is what you’ll use.

Planning Takeaway:

If the standard deduction increases for 2026, that slightly lowers your taxable income baseline. That’s good, but don’t assume it offsets a big income increase.

2026 Tax Brackets: The Important Part

Here’s what most people misunderstand:

Being “in a higher tax bracket” does NOT mean all your income is taxed at that rate.

Tax brackets are progressive.

Example: If part of your income falls into a higher bracket, only the portion above the threshold is taxed at the higher rate.

So when brackets shift upward in 2026:

- You may be able to earn slightly more before moving into the next bracket.

- That can reduce your effective tax rate.

- It may impact estimated tax payments.

What This Means for 1099 Workers

If you’re self-employed, tax bracket updates affect you more than W-2 employees.

Why?

Because:

- You control your deductions.

- You manage quarterly payments.

- You can influence your taxable income.

Here’s how to think about 2026 planning:

1. Adjust Your Quarterly Estimates

If bracket thresholds increase, you may not need to send quite as much in estimated payments — but only if income stays similar.

If income increases?

That bracket adjustment may not matter.

2. Watch Your Marginal Rate

If you’re near the top of a bracket, small strategic deductions (equipment, retirement contributions, timing expenses) can keep you from spilling into the next bracket.

3. Consider Retirement Contributions

Bracket changes make retirement contributions even more strategic.

Lower taxable income.

Lower bracket exposure.

Long-term wealth building.

4. Plan for Income Growth

If 2026 is a growth year for you, the bracket adjustment will likely be smaller than your income jump.

More revenue = higher taxes. Even with bracket increases.

Should You Change Your Strategy Because of 2026 Updates?

Usually, the updates are incremental, not dramatic.

But they should trigger a review.

Ask yourself:

- Is my income increasing in 2026?

- Am I close to a bracket threshold?

- Should I accelerate or delay income?

- Should I increase retirement contributions?

- Am I tracking deductions aggressively enough?

Tax planning isn’t about reacting in April. It’s about adjusting in January.

The Bigger Picture

The standard deduction and bracket updates are not “tax breaks.”

They are inflation adjustments.

They won’t transform your tax bill.

But they can influence smart strategy if you:

- Know your projected income

- Understand your marginal bracket

- Track expenses properly

- Use tools that show your tax exposure in real time

That’s the difference between guessing… and planning.

Final Thought

If you’re self-employed, the 2026 standard deduction and tax bracket updates are not something to skim past.

They are small levers that affect:

- Quarterly payments

- Retirement strategy

- Deduction timing

- Cash flow

Used intentionally, they help you keep more of what you earn.

Ignored? They just become another April surprise.

Disclaimer

This content is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and enforcement practices change, and individual situations vary. Always consult a qualified tax professional for advice specific to your situation.

Leave a Reply